Captive Insurance for Industrial Companies: How to Turn Rising Premiums Into Strategic Control?

Gestión de Riesgos

10 feb 2026

Your broker delivers the news: "We can't cover that risk anymore." Or worse—they can, but only at triple last year's premium with half the coverage. For industrial companies managing complex contractor networks, this isn't a hypothetical. It's the new normal.

The answer isn't to negotiate harder with your broker. It's to redesign risk financing from the inside out—through a captive insurance company that you own, control, and operate as a strategic asset, not an expense.

Key Highlights:

Why captive insurance has become essential infrastructure for industrial manufacturers?

What operational challenges come with running one?

How to build the back-office systems that turn captive strategy into execution?

What Is Captive Insurance (And Why It’s Back in Focus)?

A captive insurance company is an insurance subsidiary owned by the insured, created to pay its own losses and give owners greater control over risk and risk financing. Captives are an alternative risk transfer mechanism—not opposed to traditional insurance, but a complement that offers unbundled pricing, granular underwriting access, and direct insight into how risk management practices affect premiums.

Captives can:

Provide tailored coverage aligned to the group’s risk profile and appetite.

Retain underwriting profits and investment income within the organisation.

Improve cash‑flow management by smoothing premium flows over time.

Create potential tax and capital efficiencies, depending on jurisdiction and structure.

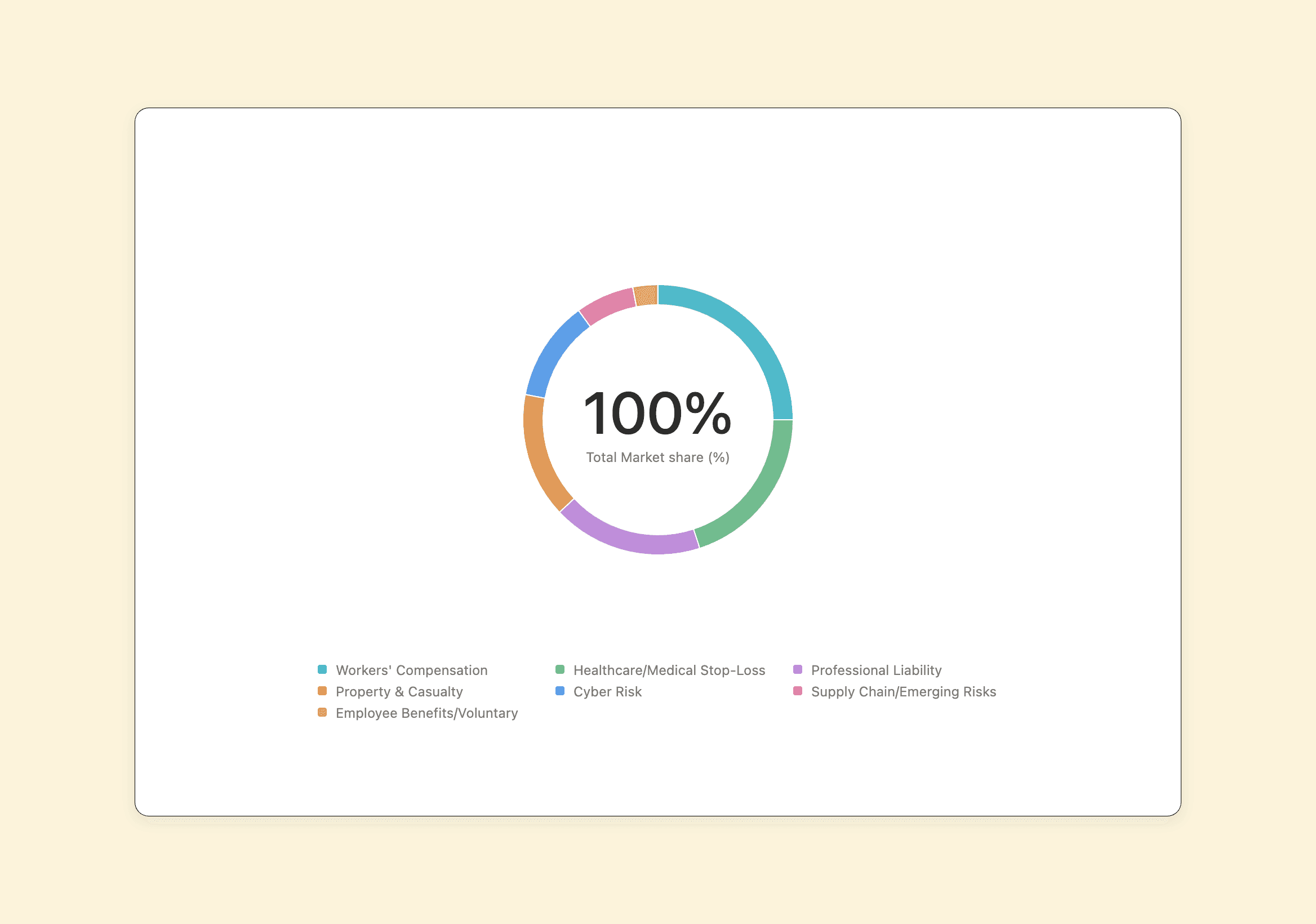

Image: Market share by sector for captives

The captive insurance market is distributed across seven primary risk categories:

Workers' Compensation (25%) – The largest segment, driven by predictable loss patterns and regulatory requirements

Healthcare/Medical Stop-Loss (20%) – Protecting self-funded employer health plans from catastrophic claims

Professional Liability (18%) – E&O, D&O, and specialized professional indemnity coverage

Property & Casualty (15%) – General liability and property damage exposures

Cyber Risk (12%) – Fast-growing segment as traditional carriers restrict coverage

Supply Chain/Emerging Risks (7%) – Novel exposures commercial markets won't underwrite

Employee Benefits/Voluntary (3%) – Supplemental benefits and group coverage programs.

Hard Market Conditions Drive Captive Growth

Traditional insurers are walking away from the risks manufacturers need covered most. Commercial casualty premiums have climbed for 31 straight quarters—the longest run in two decades. Umbrella and excess layers, the safety net for catastrophic claims, jumped 20–25% annually at their peak and still hit double digits for industrial buyers.

Workers' Compensation markets face the pressure: nuclear verdicts in injury cases and medical cost inflation have pushed carriers to restrict capacity, increase deductibles, and walk away from entire industries they deem too volatile to model profitably.

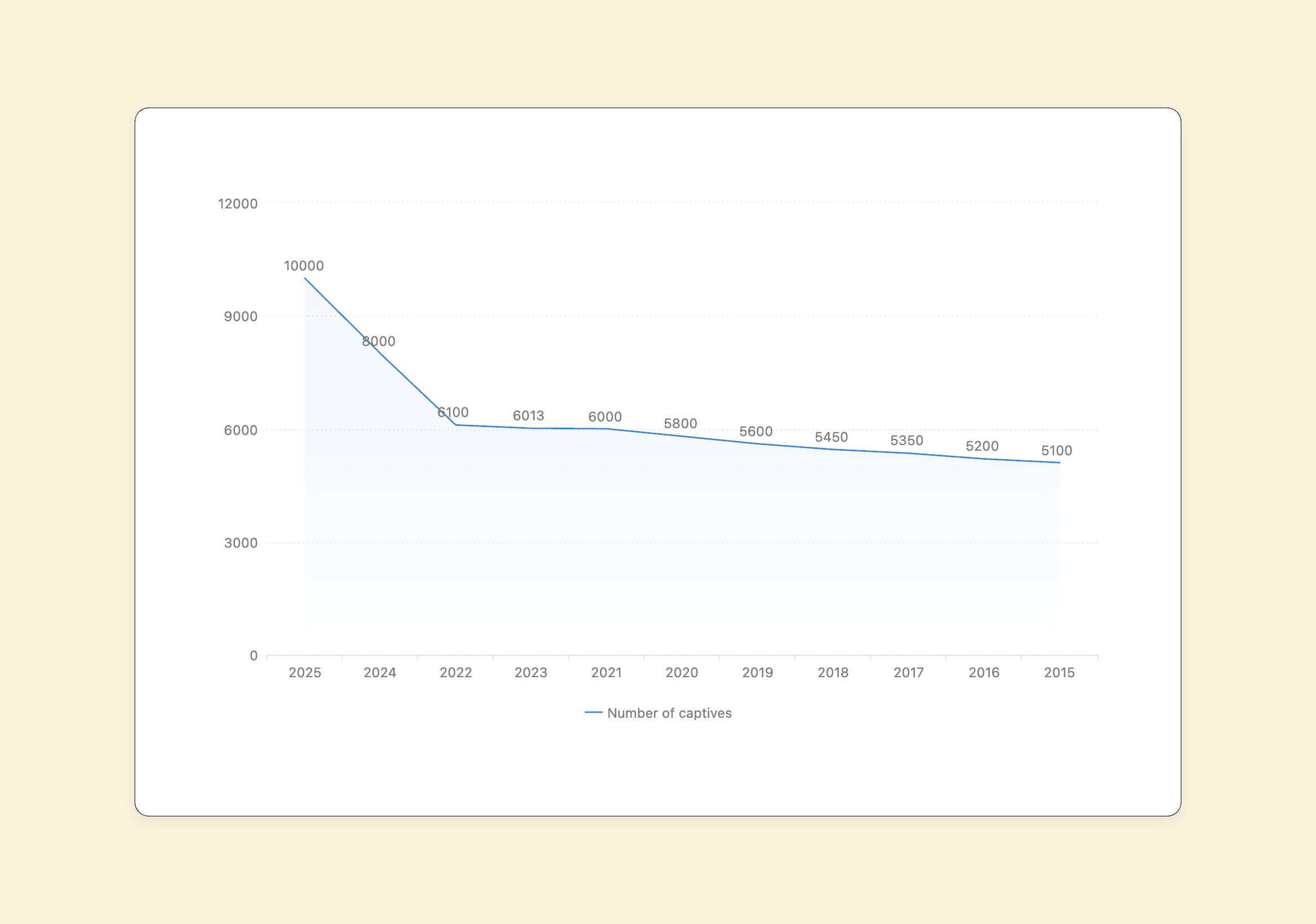

The US captive market has grown from ~5,100 captives in 2015 to 10,000+ in 2025, driven by hard market conditions, escalating premiums, and reduced capacity in traditional General Liability (GL) and Workers’ Comp (WC) markets. The result? Coverage narrows, exclusions multiply, and industrial buyers face a market that charges more while covering less.

Image: US Captive Growth (2015–2025)

That's not just numerical expansion; it represents a fundamental shift in corporate risk strategy. Companies that once viewed captives as niche tax vehicles for stable, predictable exposures now use them as primary insurance engines covering GL, WC, and emerging risks that commercial markets won't touch. Manufacturing, construction, and logistics firms are particularly aggressive adopters—sectors where contractor networks create dense third-party exposure and traditional insurers see only downside.

Why More Companies Are Building Captives? The Shift to Self-Insurance

With rising insurance costs, capacity restrictions and a surge in cyber, geopolitical and ESG‑driven liabilities, more companies are rethinking their dependence on volatile commercial markets and turning to captive (re)insurance as a core pillar of resilience. Captives can bridge this coverage gap in three ways:

Bespoke wordings – The captive can be structured to cover very specific operational and strategic risks that standard policies will not underwrite.

Deeper risk insight – Internalising the insurance function forces the organisation to understand and quantify its own risk exposures more precisely.

Financial upside – By taking on these risks in a disciplined way, the group can retain underwriting profits and potentially generate significant investment returns on captive reserves.

The global captive insurance market's growth trajectory from $79.10 billion in 2024 to a projected $120.03 billion by 2034, with approximately 10,000 risk-bearing entities globally writing $62 billion in direct premiums annually.

Source: https://www.captive.com/news/captive-insurance-2025-year-in-review-growth-risk-and-resilience

Main Challenges of Captive Insurance for Industrial Sectors

Captives used to be simple: they retained straightforward, predictable risks within a parent company's own operations. Now they've evolved into sophisticated risk-transfer vehicles managing third-party exposures across General Liability and Workers' Compensation—covering contractors, subcontractors, suppliers, and entire vendor ecosystems.

This shift means captives can no longer operate like passive holding companies. Instead, they must function like disciplined insurance carriers:

running structured processes to prequalify vendors,

govern coverage terms and exceptions,

track claims for continuous improvement,

and produce audit-ready compliance reporting.

What was once a back-office tax strategy has become a front-office operating system—and most captives are still running it with spreadsheets, email threads, and institutional memory instead of purpose-built infrastructure.

Industrial captives let manufacturers and heavy industries self-insure specialized risks—building custom coverage, capturing underwriting profits, and stabilizing cash flow instead of paying volatile premiums to commercial carriers. But managing a captive creates persistent operational challenges:

Challenge #1: Inconsistent Vendor Qualification

Industrial captives struggle to set and enforce uniform standards for financial health, safety performance, insurance adequacy, and operational capacity across complex vendor ecosystems.

Common problems:

No structured intake process—vendors submit incomplete documentation

Manual validation of COIs, licenses, and financials creates delays and errors

Unclear approval authority between corporate risk teams and project managers

Challenge #2: Opaque Underwriting and Exception Management

Tracking coverage terms, limits, deductibles, and exceptions becomes unmanageable when bespoke policies can't be mapped back to vendor controls.

Common problems:

Requirements scattered across emails and spreadsheets with no clear ownership

Missing evidence discovered late in the approval process

Exceptions granted verbally with no audit trail or expiration tracking

Challenge #3: Reactive Risk Monitoring

Without continuous oversight, compliance artifacts expire, vendor financial health deteriorates, and safety performance declines—all invisible until a claim surfaces.

Common problems:

Static vendor inventories that become outdated immediately

Manual tracking of renewals and expirations leads to lapses

Claims and incidents documented separately from vendor profiles, breaking learning loops.

Solution? Make Vendor Risk Legible with a System of Record for Captive Operations!

Captive insurance gives industrial firms control over specialized risks, underwriting profits, and cash flow—but vendor risk management creates back-office overhead. With the right risk management platform, you can convert that complexity into structured data, repeatable workflows, and measurable compliance, so operations teams can cut costs, improve governance, and scale.

Parakeet is the workflow layer that makes prequalification, underwriting, and monitoring documented, auditable, and measurable.

How Parakeet Solves Core Captive Operations

Parakeet transforms captive back-office operations across five critical areas:

Risk financing leadership requires board-ready decisions backed by current data, not stale spreadsheets. Parakeet provides standard intake processes, durable evidence storage, and complete decision trails so executives can answer "who approved what and why" in seconds instead of days.

Prequalification and due diligence ensures only qualified vendors get activated in your captive program. Parakeet maintains a requirements library, automates evidence collection, and manages approvals with built-in escalation paths—eliminating the chaos of email-based vendor onboarding.

GL and WC integration ties coverage terms directly to vendor controls and exposure data. Parakeet creates vendor profiles that centralize insurance certificates and safety artifacts, then tracks controls and exceptions over time so underwriting decisions always reflect current risk.

Regulatory and reporting burden demands that registers and reports are accurate, timely, and consistent. Parakeet maintains a living inventory with structured fields and exportable reporting inputs, turning compliance from a monthly scramble into an automated output.

Talent gaps and turnover no longer erase institutional memory. Parakeet serves as your system of record with clear workflows that survive personnel changes, ensuring processes run consistently regardless of who's in the role.

✅ Captives win when vendor risk becomes legible. Parakeet makes vendor risk legible by converting it into workflows, decision records, and structured data.

Your captive deserves an operating system as smart as your strategy. With Parakeet, you will reduce operational burden, improve underwriting confidence, and make vendor risk legible. Contact our risk experts!