Why Continuous Subcontractor Oversight Is Now a Renewal Requirement for SDI Program

Gestión de Riesgos

10 mar 2026

Jowanza Joseph

CEO, Parakeet Risk

Every Subcontractor Default Insurance (SDI) program is designed to protect general contractors from losses arising when a subcontractor defaults on its obligations — but today, those programs are operating in a market undergoing a structural shift.

Your Subcontractor Default Insurance (SDI) program protects you when a subcontractor fails to deliver — but keeping that protection is getting harder. With 70% of risk managers reporting rising subcontractor distress and claim notices up 58% since 2021, carriers now require verifiable, continuous oversight before they renew.

Introduction to Subcontractor Default Insurance

Subcontractor failures affect construction projects each year, exposing general contractors to major financial and operational risks.

Subcontractor distress is a growing threat across the construction industry —72% of construction projects face delays tied to labor and subcontractor shortages.

(Source: AGC)

Construction risk managers reported an increase in subcontractor defaults, with nearly half experiencing actual project cancellations or delays as a result, underscoring the need for robust third-party risk assessment in construction to evaluate contractors and subcontractors systematically.

📗 Read: A practical guide to Subcontractor Default Insurance, essential for informed decision-making.

Subcontractor Default Insurance is designed to protect general contractors from losses arising when a subcontractor defaults on its obligations.

However, according to Procore Technologies, SDI policies are expected to become more expensive and may require higher deductibles, which increases the value of risk automation for construction management when resolving subcontractor defaults and supporting more reliable project outcomes.

👉 Explore: Procore and Parakeet integration for smoother risk management.

In today’s construction industry, SDI is essential for protecting profitability and reputation, making it a core part of risk management. SDI does not provide first-dollar coverage for losses, making it a type of self-insurance for catastrophic losses.

SDI vs Performance Bonds

The fundamental distinction between SDI and performance bonds lies in the relationships they create. Performance bonds involve a three-party relationship between the contractor, the subcontractor, and a surety company, while SDI involves only two parties: the insurer and the insured general contractors. The claims process for SDI is faster and more reliable than that of performance bonds. That's why general contractors typically purchase SDI as an alternative to performance bonds to manage subcontractor risks.

The Prequalification Imperative: Vetting, Monitoring, and the New Rules of SDI Renewal

General contractors must vet their subcontractors to verify they can complete their assigned work and are financially stable. This means having enough resources to evaluate them carefully and keep monitoring their performance.

Subcontractor Default Insurance (SDI) helps general contractors manage and reduce the risks that come from subcontractor defaults. It provides financial protection and supports project completion, especially for projects with large or unusual subcontract amounts.

For general contractors approaching SDI renewal, the old playbook — annual prequalification checks and static spreadsheets — is no longer sufficient. Carriers now price to provable controls, and contractors who cannot demonstrate real-time monitoring, documented mitigation efforts, and a living prequalification program face:

premium increases,

coverage restrictions,

or outright non-renewal.

SDI can assist general contractors in managing and mitigating risks arising from subcontractor defaults. When prequalifying subcontractors, general contractors should look at their experience, financial health, safety record, past working relationships, and management team. Applying a structured, risk-based contractor prequalification process ensures that only those who meet these standards should be included in an SDI policy. By closing risk gaps and ensuring reliable outcomes, SDI creates peace of mind for contractors.

Understanding SDI Policies

One subcontractor default can devastate your project timeline and put your financial stability at risk. SDI policies shield general contractors from this exposure, but you need to understand the details to make smart risk management decisions.

Most policies hit you with a deductible—typically $350,000 to $2 million—that's your responsibility before insurance kicks in to cover losses. Many SDI policies also include co-pay arrangements where you share costs with the insurer.

🟩 For instance:

Your policy might cover 80% of losses while you handle the remaining 20%. This structure gives you control over policies that match your specific project types, risk tolerance, and operational needs.

Carefully choosing deductible amounts and co-pay percentages ensures the policy fits your project needs and risk tolerance. The right SDI coverage keeps your projects running smoothly and your business financially secure.

SDI policies typically require deductibles ranging from $350,000 to $2 million.

With this understanding of SDI policies, it's important to examine the current market landscape and the factors driving change.

The State of the SDI Market: Growth Amid Rising Risk

The global SDI market expanded from $3.61 billion in 2024 to an estimated $3.81 billion in 2025, and is projected to reach $5.67 billion by 2032 at a compound annual growth rate of 5.79%. SDI is typically sold to larger contractors as an alternative to surety and performance bonds to manage subcontractor risks, much like how captive insurance helps industrial companies respond to rising premiums. This growth reflects both increasing adoption by general contractors seeking alternatives to surety bonds and a risk environment that demands more sophisticated coverage structures.

Carrier Landscape: Why Subcontractor Vetting Matters More Than Ever?

Many subcontractors are now financially unstable—they don’t have enough cash reserves to handle late payments or sudden costs, like a big price jump in materials. This puts your whole project at risk if a subcontractor can’t pay their workers or finish their job.

For example, if a subcontractor’s “cash on hand” is low, even a short payment delay could cause them to walk off the job.

That’s why SDI insurers now require general contractors to check things like financial statements and past project performance before hiring. Tightening your vetting process—such as reviewing credit scores and checking references—can help you catch red flags early and avoid expensive project disruptions.

📊 Market Insights:

WTW’s Insurance Marketplace Realities 2025 reported SDI rate movements of flat to +5%. It indicates a market that, while not in hard-market territory, is becoming more selective about which programs merit favorable terms. The broader construction insurance market is experiencing a mixed environment: property rates are softening in many segments, but casualty lines — particularly excess liability — continue to see increases of 8% to 15%. Commercial general liability (CGL) premiums rose 1% to 9% throughout 2025.

Why Are Premiums Going Up?

Subcontractors are facing more financial trouble, causing insurance prices to rise. Payments are coming in much slower, which makes them even less stable. Because of this, general contractors must check subcontractors’ finances more carefully before getting SDI coverage.

💡 Market Insights:

The electrical subcontractor sector has been particularly hard-hit, with AXA XL noting a 15–18% rise in defaults within just 12 months, following a 58% spike in claim notices from 2021 to 2022.

The financial indicators are stark:

Net margins dropped 38% across all trades since 2020, and by 50% in the electrical sector

Days of cash on hand declined by 37–48%

Payment delays now average 56 days — nearly double the GC-expected 30 days

These metrics describe a subcontractor population that is increasingly fragile, with less cushion to absorb project disruptions, material price spikes, or payment delays. The financial stability of subcontractors is a significant concern for general contractors, and vetting subcontractors to ensure they are financially sound and capable of completing their scopes of work is essential to obtain an SDI policy.

Why Subcontractor Risks Are Growing?

Several macroeconomic forces are amplifying subcontractor distress and, by extension, SDI claim exposure echoes broader 2025 manufacturing supply chain disruption trends.

Material cost escalation

Prices for building materials are still much higher than before the pandemic, and new tariffs have made equipment more expensive.

Construction material prices remain over 40% above pre-pandemic levels. The Turner Building Cost Index showed a 3.64% year-over-year increase as of mid-2025.

Section 232 tariffs on steel and aluminum, and Section 301 tariffs on Chinese-origin goods, have driven up the prices of specialized equipment and components critical to large-scale infrastructure projects.

Labor shortages

There aren’t enough skilled workers, so projects are delayed and wages go up. The U.S. construction industry needed an estimated 439,000 additional workers in 2025 to meet project demands. This shortage has been compounded by an aging workforce and competition from other sectors, pushing labor costs higher and extending project timelines.

Rising interest rates

Higher interest rates make borrowing money tougher for subcontractors. Tighter credit markets have constrained subcontractor access to financing. Many subcontractors have seen credit lines non-renewed or restructured at higher interest rates, limiting their ability to manage cash flow through project cycles.

Fixing subcontractor failures is now often three times as expensive as the original contract. SDI helps protect contractors from these risks and gives them a plan to handle problems when they happen.

Most SDI policies require:

A formal declaration of default with documented mitigation efforts before coverage activates

Real-time recordkeeping including daily reports, cure notices, and schedule updates

Proof of loss submissions with complete transactional backup for all claimed amounts

Evidence that the general contractor followed subcontract default provisions before declaring default

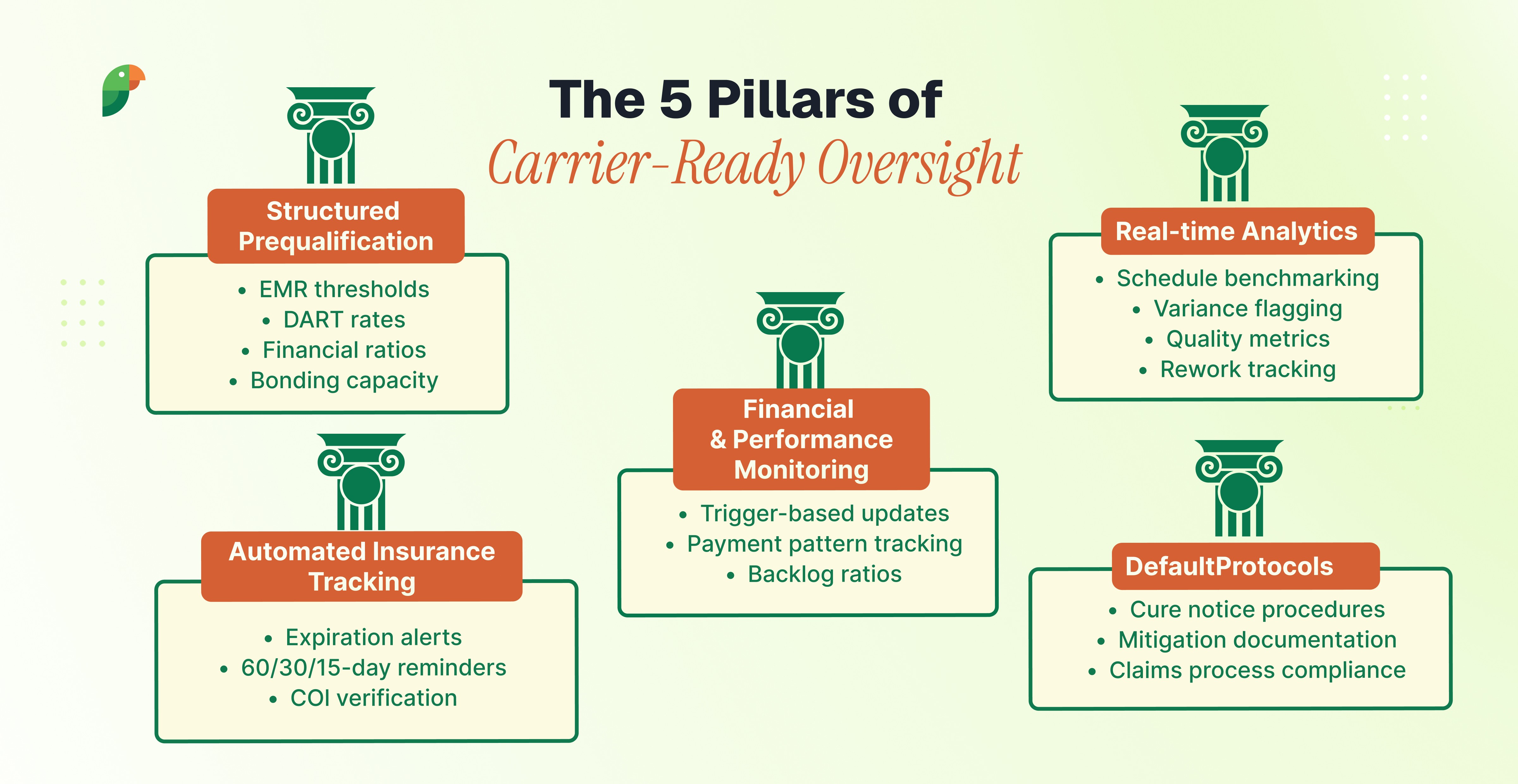

The Five Pillars of Building a Carrier-Ready Risk Management Oversight Program

A subcontractor oversight program that meets current carrier expectations should be built on five interconnected pillars:

1. Structured Prequalification with Defined Thresholds

Make simple, clear rules for picking subcontractors — EMR thresholds, DART rates, financial ratios, bonding capacity, and experience requirements — and apply them consistently across all subcontractor tiers. Check facts with real data instead of just trusting what subcontractors say. Keep all records in one place so that if a subcontractor fails on one job, they can't sneak onto another project.

2. Automated Insurance Compliance Tracking

Stop tracking Certificates of Insurance (COIs) by hand. Use automated systems to check expiration dates, send reminders before coverage ends, and block site access if insurance lapses. Make sure subcontractors have sufficient coverage and the right endorsements to keep your business protected.

3. Ongoing Financial and Performance Monitoring

Besides yearly financial reviews, set up risk alerts for major company changes, late payments, or big shifts in workload. Watch early warning signs—not just past safety records—and compare work completed to what’s been billed. This helps spot financial problems in subcontractors before they get worse.

4. Real-Time Schedule and Quality Analytics

Carriers have invested heavily in schedule benchmarking because schedule delays are often the first sign that a subcontractor is struggling. Use scheduling tools to spot these delays early, compare progress to your plan, and act before issues get worse. Adding AI tools and tracking things like rework and failed inspections gives you even more warning when problems start.

5. Documented Escalation and Default Protocols

Make sure your subcontractor contracts clearly state what happens if there’s a problem, including how and when you’ll notify them and give them a chance to fix it. Keep good records showing how you followed these steps. Insurance companies will check your paperwork to see if you followed the contract rules before approving any SDI claim. The SDI claims process begins with the provisions of the subcontract agreement — and the carrier's assessment of your claim begins with whether you followed those provisions.

Implementation of Continuous Oversight

If a subcontractor fails, it can ruin your project and reputation. Many contractors can't see problems early because they aren't tracking subcontractor performance in real-time. Using AI-powered risk management platforms like Parakeet helps detect and address issues early, avoiding delays and extra costs.

According to Hudson Insurance:

Implementing Subcontractor Default Insurance gives general contractors greater control and flexibility, helping them complete projects on time and within budget, which supports long-term resilience and success.

Taking a proactive approach not only lowers risks but also improves teamwork and fits with how big companies safely manage their suppliers, which is crucial for industrial global supply chains that require constant monitoring across all tiers.

📗 Read about the role of supply chain management in modern manufacturing processes.

What is the Future of the Construction Industry?

The future will favor construction leaders who can adapt to new technologies, leverage AI-driven insights for decision-making, and build resilient supply chains. Staying updated on industry trends and always improving your processes will protect your business financially and help avoid preventable losses.

❇️ For more perspectives on evolving risk, technology, and regulation, explore the Parakeet Risk insights blog.

Insurers now want proof that you are always monitoring your subcontractors. Using real-time data, making it easy for new suppliers to join, and staying on top of changing rules are all key to keeping your insurance and controlling costs.

Careful vetting is not just smart—it’s required if you want SDI coverage. Want to protect your projects? Start by reviewing your subcontractor screening process today. Contact our experts to learn more! 🦜